Trump’s Reciprocal Tariffs Shock Markets

April 05

Hello Traders, we hope you’re having a nice weekend. Here are some of the biggest stories this week:

Dig deeper into these stories in this week’s review.

The EU and Canada retaliated against US President Donald Trump’s 25% tariffs on steel and aluminium within hours of them taking effect on Wednesday, escalating a trade war that has unsettled financial markets and threatened the global economy. The European Commission said that its measures would target up to $28 billion worth of American goods – matching the US tariffs on European exports – and would take effect in April, allowing time for negotiations with Trump. The levies, which Trump vowed to respond to, impact a wide range of products, from bourbon whiskey and Harley-Davidson motorcycles to soybeans and other agricultural goods. Canada, meanwhile, also retaliated by announcing new 25% tariffs on about $21 billion of American goods, including US steel and aluminum products as well as consumer items such as computers and sporting goods.

According to a new report by the Institute of International Finance this week, global debt increased by around $7 trillion in 2024 to reach a record $318 trillion. What’s more, total debt as a share of global GDP rose for the first time in four years, as economic growth slowed in many parts of the world. Pointing toward those rising debt burdens, the IFF said that governments should beware of “bond vigilantes” – the term given to investors who push up yields in a bid to force policymakers to rein in budget deficits and debt. Speaking about the US specifically, the institute noted that strong economic activity, productivity growth, and the safe-haven status of US Treasuries are overshadowing increasing weaknesses in the US’s fiscal balances.

This all matters since escalating global debt levels, coupled with increasing fiscal vulnerabilities in the US, could potentially destabilize markets. That’s because investors may demand higher yields on bonds to compensate for perceived risks, leading to tighter financial conditions worldwide. And this is already happening, with bond yields in several major economies, from Europe to Japan, surging this year.

New data this week showed the UK economy unexpectedly shrank at the start of 2025, with GDP contracting by 0.1% in January from the month before – below both the 0.1% growth predicted by economists and December’s 0.4% expansion. The decline, which was mainly driven by the manufacturing and construction sectors, means that the economy has contracted in four out of the past seven months. While analysts anticipate a return to steady growth this year, risks to the outlook are mounting, with Trump’s escalating trade war rattling markets and fueling fears of a global downturn. But hopes remain that Britain’s planned surge in infrastructure spending will help support growth in the near term…

US inflation fell more than expected in February, strengthening the case for the Fed to cut interest rates amid signs of slowing growth in the world’s biggest economy. Consumer prices increased by 2.8% last month from a year ago – slightly less than the 2.9% economists had predicted and a marked deceleration from January’s 3% pace. Core inflation, which strips out volatile food and energy items to give a better idea of underlying price pressures, fell from 3.3% in January to 3.1% in February – better than the 3.2% economists had expected. On a month-over-month basis, both headline and core inflation came in at 0.2%.

Traders slightly raised their bets for Fed interest rate cuts following the report. The central bank faces a difficult balancing act as it tries to bring down inflation without triggering a recession, amid intensifying fears that Trump’s aggressive economic agenda is hampering growth. For now, the Fed is patiently sitting in wait-and-see mode until there’s more clarity on the administration’s actions and the inflation trajectory, with officials widely expected to keep rates steady at next week’s meeting.

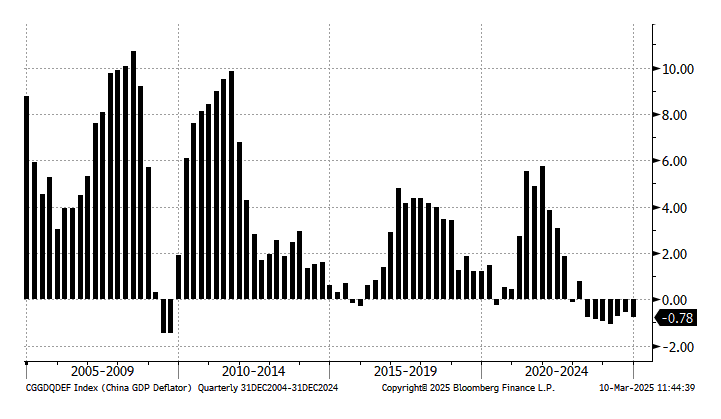

New data this week showed Chinese inflation in February fell more than expected, dropping below zero for the first time in 13 months. Consumer prices declined by 0.7% from a year ago – much worse than the 0.4% drop economists had predicted and marking a sharp contrast to January’s 0.5% gain. Investors need to take the report with a grain of salt, however, as seasonal distortions may have influenced the data. More specifically, the statistics office said that the earlier-than-usual lunar new year holiday was the main reason for the decline. See, prices tend to increase during the holiday, which falls on a different date every year, as consumers spend more on travel and food. The holiday started on January 29 this year, compared with February 10 last year, and the statistics office estimated that consumer prices actually rose 0.1% when adjusted for the lunar new year shift.

Nonetheless, other parts of the report were worrisome. Core inflation, which strips out volatile food and energy items to give a better idea of underlying price pressures, dipped below zero for the first time since 2021. What’s more, producer prices, which reflect what factories charge wholesalers for products, fell for the 29th consecutive month, dropping by a bigger-than-expected 2.2% in February.

Taken altogether, the figures provide further evidence of weak consumer demand in the world’s second-biggest economy, prompting calls for additional measures to prevent a negative cycle of falling prices and declining activity. See, anticipating further price drops, consumers might delay purchases, dampening already weak consumption. Businesses, in turn, might lower production and investment because of uncertain demand. What’s more, falling prices lead to lower corporate revenues, potentially hitting wages and profits. Finally, during times of deflation, prices and wages fall, but the value of debt doesn’t, which adds to the burden of repayments and raises the risk of defaults.

Next week

General Disclaimer

This content is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell. Investments carry risks, including the potential loss of capital. Past performance is not indicative of future results. Before making investment decisions, consider your financial objectives or consult a qualified financial advisor.

Nope

Sort of

Good

%2FgRTFfWwPmcWyE8PFfywB82.png&w=1200&q=100)

%2FAD2MfhoJXohkTgrZ5YjADV.png&w=1200&q=100)

%2FjjqkumDfGjhNxroL253Hc4.png&w=1200&q=100)